What is the Europe Flatbread Market Overview – definition, scope, and significance?

The Europe flatbread market comprises the production, distribution, and consumption of ready‑to‑eat flatbreads such as tortilla, naan and pita across European countries. The scope covers all commercial channels – supermarkets, hypermarkets, bakeries and convenience stores – and includes both traditional and value‑added variants (gluten‑free, organic, fortified). This segment is significant because flatbreads serve as a versatile base for meals, snack solutions and ethnic cuisines, driving steady demand in a region known for diverse culinary habits and a growing preference for convenient, nutritious foods.

What are the key drivers, restraints, challenges, and opportunities shaping the Europe Flatbread Market?

Key drivers include rising health consciousness, demand for clean‑label products, and the popularity of Mediterranean and Latin American cuisines. Urbanisation and busy lifestyles boost convenience‑oriented purchases through supermarkets and convenience stores. Restraints involve raw material price volatility (wheat, cassava flour) and strict EU food‑safety regulations that increase compliance costs. Challenges stem from intense competition and the need for product differentiation. Opportunities arise from innovation in functional flatbreads (high‑protein, fortified), expansion into premium retail formats, and growing demand for plant‑based and gluten‑free options.

What are the current and emerging growth trends in the Europe Flatbread Market?

Current trends show a shift toward premium, artisanal flatbreads with authentic regional flavours, especially in bakery channels. Emerging trends include the launch of fortified flatbreads enriched with vitamins, minerals and dietary fibre, and the integration of alternative grains such as quinoa and teff. Digital‑first marketing and direct‑to‑consumer e‑commerce platforms are gaining traction, while sustainability claims (eco‑packaging, reduced carbon footprint) influence purchasing decisions across all distribution channels.

How has COVID‑19 impacted the Europe Flatbread Market and what is the recovery trajectory?

The pandemic initially disrupted supply chains and reduced foot traffic in bakery outlets, but simultaneously accelerated home‑cooking and demand for shelf‑stable flatbreads. Supermarkets and hypermarkets saw a pronounced uplift as consumers stocked up on versatile products. Recovery is now robust, with demand normalising across all channels and a continued preference for convenient, ready‑to‑eat flatbreads supporting steady growth beyond the pandemic period.

Who are the major competitors and what is the state of market consolidation in the Europe Flatbread Market?

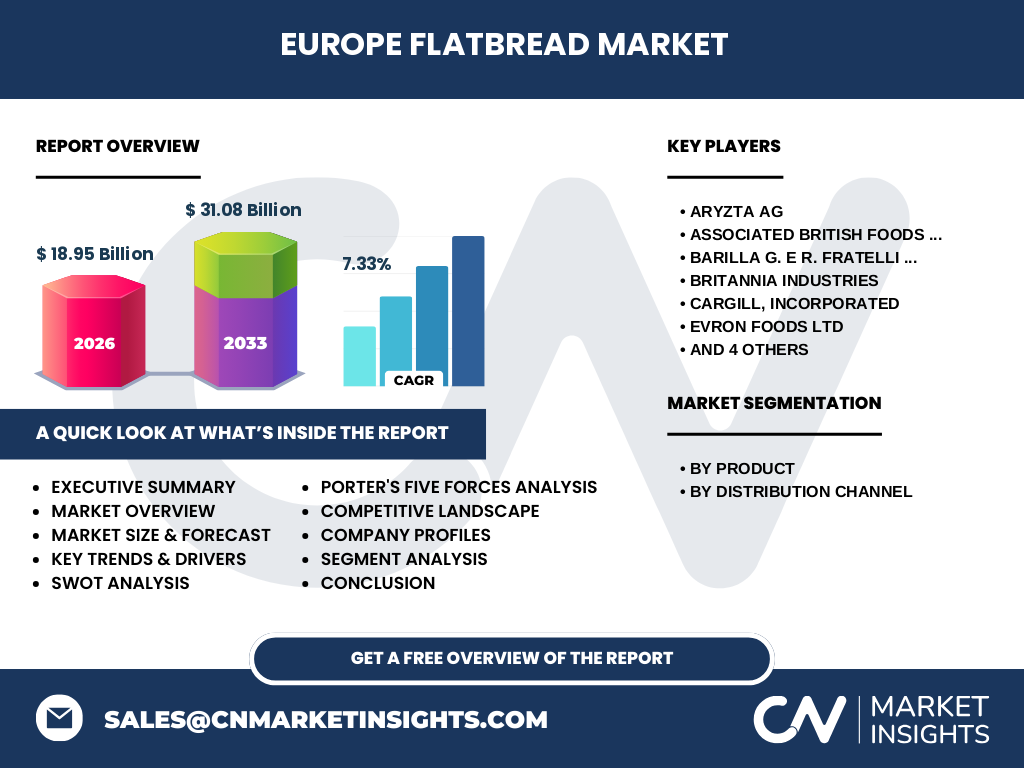

Key players include Aryzta AG, Associated British Foods plc, Barilla G. e R. Fratelli S.p.A, Britannia Industries, Cargill, Incorporated, Evron Foods Ltd, Gruma S.A.B. DE C.V, KRONOS, Kontos Foods Inc., and Rich Products Corporation. The market exhibits moderate consolidation, with large multinationals leveraging extensive distribution networks while niche manufacturers focus on specialty flatbreads. Recent strategic alliances and acquisitions indicate a trend toward strengthening portfolio breadth and expanding geographic reach.

What are the high‑level findings in the Executive Summary for the Europe Flatbread Market?

The Europe flatbread market is valued at €18.95 billion in 2026 and is projected to reach €31.08 billion by 2033, delivering a CAGR of 7.33 %. Growth is propelled by health‑focused consumer trends, convenience demand, and product innovation across tortilla, naan and pita segments. Supermarkets and hypermarkets dominate distribution, but bakeries and convenience stores also capture niche premium sales. Leading companies are investing in fortified and gluten‑free lines, while sustainability and e‑commerce are emerging as strategic differentiators.

What are the forecast expectations for the Europe Flatbread Market during 2025‑2032?

Based on the provided CAGR of 7.33 %, the market is expected to maintain a steady upward trajectory, expanding from the 2026 base of €18.95 billion to approximately €31.08 billion by 2033. This growth reflects continued consumer preference for quick‑serve flatbreads, expansion of premium product portfolios and deeper penetration of flatbreads into health‑oriented retail formats. The forecast underscores robust demand across both traditional (tortilla, pita) and emerging (naan, functional) product categories.

How is the Europe Flatbread Market sized and shared by product and distribution channel segmentation?

By product, the market is divided into tortilla, naan and pita categories, each catering to distinct culinary applications and consumer preferences. By distribution channel, sales are segmented into supermarket and hypermarket, bakery and convenience store channels. While specific monetary shares are not disclosed, the structure indicates that supermarkets/hypermarkets capture the largest volume due to broad reach, bakeries serve the premium, freshly‑baked segment, and convenience stores address on‑the‑go consumption patterns.

What is the geographic distribution of the Europe Flatbread Market at a global level?

At a global level, Europe represents a major regional hub for flatbread consumption, contributing the full market size of €18.95 billion in 2026. The region’s diversified economies, strong retail infrastructure and multicultural food habits position it as a leading consumer of tortilla, naan and pita products compared with other continents.

What does the regional analysis reveal about performance within Europe?

Western Europe – particularly Germany, France and the UK – drives the bulk of volume through extensive supermarket networks and a high propensity for convenience foods. Southern Europe (Italy, Spain, Greece) shows strong demand for traditional pita and naan, reflecting Mediterranean dietary patterns. Scandinavia and Central Europe exhibit growing interest in health‑focused flatbreads, especially gluten‑free and fortified varieties, fostering premium‑price growth in bakery and specialty channels.

Which companies lead the Europe Flatbread Market and what are their strategic initiatives?

Leading firms such as Aryzta AG and Associated British Foods plc leverage extensive bakery footprints and innovate with specialty flatbreads. Barilla focuses on Mediterranean‑style pita, while Gruma capitalises on its global tortilla expertise to expand in European retail. Cargill and Rich Products drive ingredient‑supply innovation, supporting fortified and functional flatbread formulations. Recent initiatives include product line extensions into high‑protein tortillas, sustainability‑focused packaging, and strategic joint ventures to broaden market reach.

How does Porter’s Five Forces framework apply to the Europe Flatbread Market?

• Threat of new entrants: Moderate – high capital investment in production facilities and regulatory compliance create barriers, yet niche artisanal brands can enter through boutique bakeries.

• Bargaining power of suppliers: Moderate – reliance on wheat and specialty grains gives suppliers some leverage, mitigated by diversified sourcing.

• Bargaining power of buyers: High – large retail chains negotiate aggressively on price and shelf‑space.

• Threat of substitutes: Low to moderate – alternative carb products (rice cakes, wraps) exist but flatbreads retain unique cultural and functional appeal.

• Industry rivalry: High – numerous established multinationals and local players compete on price, innovation and distribution reach.

What are the SWOT insights for the Europe Flatbread Market?

Strengths: Strong consumer familiarity, versatile applications, and robust retail channels.

Weaknesses: Sensitivity to raw‑material price swings and narrow profit margins in mass‑market segments.

Opportunities: Expansion of functional flatbreads, sustainability initiatives, and digital sales channels.

Threats: Intensifying price competition, regulatory changes, and potential supply disruptions for key grains.

How is the value chain structured in the Europe Flatbread Market?

The value chain begins with raw‑material procurement (wheat, alternative grains), followed by processing (mixing, sheeting, cooking). Next, packaging and quality‑control steps add value before products are distributed to supermarkets, bakeries and convenience stores. End‑users—retailers and ultimately consumers—drive demand, while logistics providers and ingredient suppliers play critical supporting roles in ensuring freshness and cost efficiency.

What key investment insights can be drawn for stakeholders interested in the Europe Flatbread Market?

Investors should target companies that are expanding functional flatbread portfolios, embracing sustainable packaging, and strengthening e‑commerce capabilities. Strategic M&A activity around niche artisanal brands can provide entry into premium segments. Partnerships with grain suppliers for price‑stable contracts and investment in automated processing technologies will enhance margins and support the projected 7.33 % CAGR.

What are the concluding takeaways from the Europe Flatbread Market analysis?

The Europe flatbread market is on a clear growth path, underpinned by health trends, convenience demand and product innovation. A solid base of major manufacturers combined with emerging specialty players creates a dynamic competitive environment. Continued focus on fortified, gluten‑free and sustainable offerings, alongside expansion of digital distribution, will be decisive for capturing market share through 2033.

How was the research for this market report conducted?

The study employed a mixed‑method approach, combining primary interviews with industry executives, secondary data extraction from company reports, trade publications and EU statistical sources, and quantitative modelling to project market size and CAGR. Validation steps included cross‑checking figures with independent market databases and expert panels.

What is the scope of this research and any limitations?

The scope covers flatbread categories (tortilla, naan, pita) across all European countries, focusing on the retail distribution spectrum (supermarkets/hypermarkets, bakeries, convenience stores). It excludes off‑line institutional sales (cafeterias, schools) and does not quantify individual country‑level market shares due to data availability constraints.

Which key companies are highlighted and what recent developments have they announced?

Prominent companies include Aryzta AG (new gluten‑free pita line), Associated British Foods plc (strategic acquisition of a regional bakery network), Barilla (launch of organic tortilla range), Britannia Industries (partnership with a plant‑based ingredients supplier), Cargill (investment in sustainable grain sourcing), Evron Foods Ltd (expanded capacity in Eastern Europe), Gruma (introduction of high‑protein tortilla), KRONOS (launch of eco‑friendly packaging), Kontos Foods Inc. (digital direct‑to‑consumer platform) and Rich Products Corporation (collaboration on fortified flatbread formulation). These initiatives reflect a market shift toward health, sustainability and digital engagement.